The RBI has recently experimented the monetary policy method of Operation Twist. It has conducted three rounds of Operation Twist– on December 19th 2019, December 23rd, 2019 and 6th of January 2020. Here we are examining the meaning of operation twist, its working and implications on the economy.

What is Operation Twist?

Operation twist is a monetary policy intervention by the central bank, conducted through Open Market Operations (OMOs), where the central bank is buying long term bonds of the government and at the same time selling short term securities of the government. Buying long term securities and selling short term securities will reduce the yield of long term securities compared to that of the short term ones. This yield impact is the objective of Operation Twist.

Also Read: What is Yield curve for a bond?

Why Operation Twist?

Lower longer-term yields and thus the reduced long-term interest rate will support the economy by making loans less expensive to buy homes, cars, and to finance investment projects.

Operation twist is conducted through open market operations of selling and buying of government securities.

|

What is Operation Twist? “Operation Twist” was famously conducted by the US Federal Reserve in 2012 to stimulate the economy. Under Operation Twist, the Federal Reserve bought long-term bonds and simultaneously sold short term securities. This was to bring down long-term interest rates. Because of simultaneous buying and selling of two different types of securities, there occurs a “twist” in the shape of the yield curve. The term “Operation Twist” was first used in 1961 by the Federal Reserve. |

What are the objectives of Operation twist?

RBI’s operation twist is not as powerful or ambitious like the one done by the US Federal Reserve in 2012. Don’t forget that the monetary policy transmission mechanism is not fine-tuned as in the US. More than anything else, the happy feeling that it can influence long term yield itself will be a confidence boosting outcome for the RBI as it is test-firing this equipment.

The first objective is to reduce the yield of the long-term government securities. The real benefit of such a step is that the government need to pay only lower interest rates if it issues more securities in future as part of the borrowings. Given the current yield is lower, it may make mor comfort for the government to issue long term securities in future.

The second objective is to bring down long term interest rate so that higher credit, consumption, investment etc. can go up.

Thirdly, the RBI is tired of using the repo rate without much result. The central bank is complaining that banks are not following the repo signal by adjusting their lending rates. In this context, the RBI was searching for new instruments of monetary policy transmission. The operation twist is test of a new option through which the RBI can influence market interest rate by selling and purchasing government bonds.

|

Operation Twist and its connection with the forthcoming budget The next budget (to be presented on February 1st, 2020) will be a critical one for the government as it is going to make heavy borrowings to support the expenditure. This is because stagnating tax revenue is a major problem at present. Here, if the government makes high borrowings (indicated by a higher fiscal deficit), the interest rate (yield) it has to give will increase. Higher the borrowing, higher will be the upward pressure on the market interest rate. That is the way fiscal deficit works on the market yield of government securities. This is because, higher volume of government securities can be sold only if higher interest rate (yield) is offered. Here comes the significance of the Operation Twist. As the central bank has purchased lot of government bonds, the yield fell, and it will be comfortable for the government to sell its securities because market yield for government bonds has come down. So, operation twist is facilitating government borrowing and thus the next budget in indirect and critical way. |

What is Open Market Operations (OMOs)?

Open Market Operations refers to the selling and buying of government securities. When the RBI sells the government securities, the securities goes to the public and equivalent money goes to the central bank and thus finally to the government who is the owner of the securities.

On the other hand, when the RBI buys the government securities, money goes to the public and securities goes to the RBI.

Another outcome of the OMOs is the interest rate or yield effect. Here, when the RBI buys the securities, the demand for that securities goes up and hence, and their price goes up resulting decline in yield.

There are two types of government securities in terms of maturity. First is the long-term securities or what we call government bonds. They have maturities of 5-year, 10-year, 20-year etc.

Second, there is the short-term securities or what we call Treasury Bills. They have a maturity period of maximum 364 days (or less than one year).

A ten-year government bond, that has completed nine year now and has a residual maturity of 1 year can be considered as a short-term bond as of today.

|

How decline in the yield of long-term government securities will help the economy? Government securities are benchmarks for the financial system. This means that several financial institutions set their interest rate on long term loans based on the yield of long-term government securities. When the yield of long-term government securities comes down, financial institutions will reduce interest rate on long term loans. Additionally, the reduced yeild will help the government to sell its newly issued bonds at a comfortabel or moderate interest rate. |

How selling and buying of securities by the RBI affects their yield?

When there is a high demand for a government security, (due to RBI buying) its price increases.

Imagine that the price of ten-year bond was originally Rs 1000 (with an interest rate of 10% or Rs 100).

Suppose there is high demand for 10-year government bonds, because of high buying by the RBI.

As a result of high level of RBI borrowing, demand increases their price in the (secondary market for bonds) goes up to Rs 1200. Amidst high demand, people are ready to sell the bond only at a higher price. Here, the price of a Rs 1000 bond increases to Rs 1200 in the secondary market. The secondary market is the market where you can sell and buy bonds like shares.

Still, a guy buying a 10-year bond gets Rs 100 as interest as the interest rate was originally set at 10% (of Rs 1000). The new owner of the bond spent Rs 1200, but he gets the interest of Rs 100 (that is the interest rate or yield he is getting from this bond). Effectively Rs 100 for a Rs 1200 investment is 8.3%. Original interest rate 10%; but in the market for that bond, the price increased, but yield decreased.

This 8.3% yield is lower than the original interest rate (yield) of 10%. Hence, here, when the RBI buys government securities, its yield falls.

Operation twist and its effect on the economy

If the RBI buys long term bonds, the yield of long-term securities comes down. This will have economy wide implications. Because several institutions charges interest rates on loans based upon the yield of government securities. Government securities are considered as financial benchmarks for other institutions to set their interest rates.

If the yield of long-term securities comes down, banks will reduce interest rate of their long-term loans. So, declining yield of government securities is a signal to the entire financial system. Similarly, the interest that the corporate should pay for their long-term bonds also will fall.

|

What is the idea behind Operation Twist? Reducing the yield on long term government securities will help to reduce interest rate on long term loans. This will encourage households and business to take long term loans to make more consumption and investment. Secondly, if the government is planning to make higher borrowings in the next budget, operation twist will help the government to enjoy a moderate interest rate, |

In essence, there will be a decline in long term interest rate when the RBI buys long term bonds. This low interest rate will encourage household and business to take long term loans to make consumption and investment thus stimulating economic activities.

On the other hand, when the RBI sells short term government securities, their price falls and their yield increases.

Under operation twist RBI:

(1) Bought long term securities and

(2) Sold short term securities.

As a result:

(1) The interest rate on long term loans will come down

(2) interest rate on short term loans will go up.

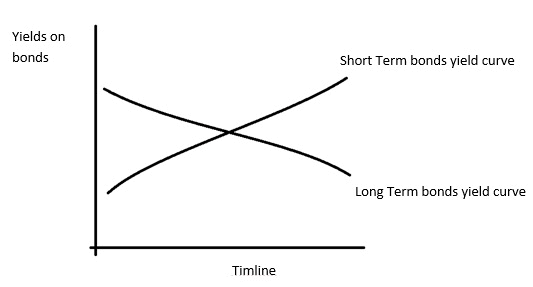

Figure: Operation Twist yield cuve impact: Yield of long term securities comes down, whereas the yield of short term securities goes up.

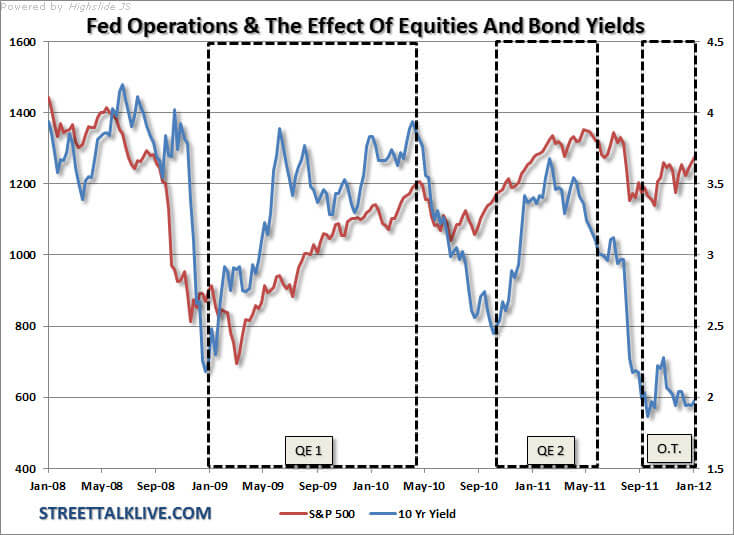

Figure (below): Yield curves when the US Federal Reserve conducted operation twist during 2011-12. (image courtesy Streettalklive.com). The 10 year yield curve is shown in blue colour whereas the S&P 500 index yield in red colour is shown as proxy for short term yield.

So, here to reduce the long-term yield of the bonds, the RBI resorted to operation twist. The objective of the RBI is to bring down the long-term cost of government borrowing and overall long-term interest rate in the economy. When the long-term interest comes down, there will be expansion of long-term credit and investment.

Whether the Operation Twist found its objectives?

Operation twist reasonably met its objectives as the data shows that the long-term yield has come down notably after the result of RBI’s Open Market Operations. At the time of the first round of operation twist, the 10-year yield was 6.75 percent and after the two rounds of Operation Twist has come down to 6.51 percent.

Operation Twist 2019-20RBI conducted three rounds of Operation Twist. The first one was on December 19, 2019. Second round on December 23rd, 2019 whereas the third one was on 6th January 2020. Round1 – December 19, 2019: Open Market Operations worth Rs 10000 crore was made by the RBI. Round 2: December 23, 2019 Buying of securities: The RBI conducted second round of Open Market Operations on 23 December. Here, the central bank purchased Rs 10,000 crore worth of 2029 long-term securities (10 year). In the second tranche, the RBI bought Rs 10,000 crore of long-term securities Selling of securities: RBI sold short-term bonds worth ₹6,825 crore (less than one-year maturity). In a second tranche, the RBI sold only Rs 8,501 crore of short-term bonds. Short term bonds are bonds with low residual maturity (less than one year etc.). It may be a ten-year bond issued in the past, but there is only less than one year remaining for it to mature. Round 3: January 6, 2020 Buying of securities: Here, the RBI purchased two new long-term government securities (bonds) maturing in 2024 and 2026. In addition to these, the central bank bought 10-year bond maturing in 2029. Selling of securities: Treasury bills (less than one-year maturity) and bonds with residual maturity of less than one year. Here, the RBI sold short-term securities including T- bills maturing on 9th April 2020, on 3rd May 2020, and on 9th June 2020. Besides bonds maturing on 10 December 2020 has also been sold. As a result of the first round of Operation Twist, the yield of the central government’s long term securities fell in the market; indicating success of the RBI’s new venture. |