Concepts related to bonds are often difficult to understand for most first-time learners. At the same time, developments in the bond market are getting more coverage and relevance in news related with the financial sector.

Concepts related with bonds

|

To understand the working of bond, you must know a lot of connected concepts. Not just concepts but also how the working of these from a practical angle. We will also see how the opearation twist works from the yield side.

The basic concepts related with bonds are: yield, interest rate, coupon interest rate or yield, maturity, bond price etc. Among this, two factors -the concept of yield and how bond prices are estimated; will help you considerably to understand the working of bonds and their connection with the economy.

Actually, you can’t understand the concept of yield without knowing about bonds and how bond prices are estimated.

What is a Bond?

Bonds and equities are two popular instruments issued by corporate to mobilize funds (in India, government bonds are more popular). If you are the owner of a company, you can mobilise funds either through issuing your company’ share to others or by issuing debt instruments (like bonds) to others.

The difference is that when you are issuing shares, you have to transfer a part of the ownership of the company to the shareholder (in most cases). But you are not a debtor (that is the positive).

Bond is a debt paper in the sense that if you are selling Rs 1000 worth of bonds, you get that amount from the bond purchaser and owe him Rs 1000. At the maturity time, you have to repay the Rs 1000 and at regular intervals you have to pay the interest.

Advantage of bond is that you are not transferring the ownership of the company. On the disadvantage side, you become a debtor.

By purchasing debt (bond), an investor becomes a creditor to the corporation (or government). Thus, a bond is like a loan: the holder of the bond is the lender (creditor), the issuer of the bond is the borrower (debtor).

The date on which the issuer has to repay the amount (known as face value) borrowed is called the maturity date.

Who issues bonds?

Corporate and governments issue bonds to mobilise money. So, there is the government bonds and corporate bonds.

To understand clearly about bonds, we have to go through some basic concepts.

Basic concepts about bonds

- Face Value of Bond: The face value of bond is commonly referred to the amount that should be paid to a bondholder at the maturity date. The face value is also known as the repayment amount.

- Coupon: A coupon payment on abond is a periodic interest payment that the bondholder receives during the time between when the bond is issued and when it matures. If bond has a face value of Rs1000 and a coupon rate of 5%, then it pays coupon amount of Rs 50 per year.

- Maturity Date: Maturity date is the date when the principal (face value) is paid back. The time to maturity can vary from short term (1 year) to long term (30 years or even perpetuities).

- Bond Price: One important factor about bond is that it can be sold and bought from the secondary market like shares. Generally, no person will be buying bonds to sell at the expiry date. Rather, bond holders are targeting to sell whenever the price of the bond they purchased goes up (like in the case of shares).

In the US, an average bond holder keeps the bond he bought for a period of 36 days (on an average). Generally, the bond holder sells the bond when he gets a higher price (like in the case of shares).

This means that you can buy and sell bonds from the secondary market (stock market) like in the case of shares.

The price at which a bond is purchased from the market or sold is called bond price. Here, the mechanism is exactly the same as the price of a share. Major difference is the way in which bond price is estimated.

The price of a bond will be near to its face value. This means that if your bond’s face value is Rs 1000, the price you may get while selling it will be somewhere around Rs 1000.

How much it differs from this face value depends upon a number of factors including the most important one – difference between the interest rate that your bond offers and the general interest rate existing in the economy. The market interest rate may change depending upon the repo rate policy of the RBI or due to other factors.

Bond prices in the secondary market can be higher or lower than the face value of the bond depending on several factors.

If we buy a new bond and plan to keep it to maturity, changing prices, interest rates, and yields typically do not affect us. Here we purchased a bond at Rs 1000, and we will get Rs 1000 at maturity.

|

How bond price is expressed? Price for a bond is important when the investor intend to trade bonds with other investors. A bond’s price is what investors are willing to pay for an existing bond. In newspapers and statements, bond prices are provided in terms of percentage of face (par) value. An example will reveal this. Suppose the investor is considering buying a corporate bond. It has a face value of Rs 10, 00. At three points in time, its price – what investors are willing to pay for it – changes from 97, to 95, to 102. This means that the buyer has to pay Rs 970 when the price is 97. Again, he has to pay Rs 950 when the price of bond is 95. In these two cases, the bond’s price has declined and hence the buyer or investor gets a discount. But when the price is 102, the buyer should pay Rs 1020 and thus there is a premium to get the bond. |

Bond Price and the prevailing market interest rate.

We saw that the most important factor that determine the price of a bond is the interest rate offered on the bond and its difference with the prevailing interest rate.

Suppose that your Rs 1000 bond is having an interest rate of 8% (coupon yield or interest rate). But the interest rate in the economy for the same time period loan declined to 6% because the RBI reduced the repo rate and banks reduced their lending rates. Here, your bond becomes attractive as it offers a higher interest rate. Understandably you are not ready to sell the bond at Rs 1000 in the market. The market will give you a higher price or a premium (RS 1000 plus or imagine Rs 1050) for your bonds. The exact price is determined in the market and you can get a premium.

The opposite will happen when the market interest rate goes up. There are several factors that determined the price of your bond. Other factors include the creditworthiness of your bond issuing entity, general liquidity in the economy etc. Still the most important one is the interest rate difference.

Also Read: What is Operation Twist by the RBI?

Yield of a bond

Yield in a literal sense is the annual percentage return earned on a security. For example, a 10% yield means that the investment averages 10% return each year. For a simple bond holder who bought it from the primary market and keeps the bond till maturity, the yield is the coupon interest rate of 10% (coupon yield). The interest income is Rs 100.

But things will be different when you purchase the bond from the secondary market. Here you may not be buying the bond at the issue price (Rs 1000). Rather may be purchasing at a discount (Rs 800) or a premium (Rs 1200).

In the case of a premium your effective return is Rs 100 (10% of Rs 1000) while spending Rs 800. Here, your yield is higher (than 10%) and is 12.50%. This is called as the current yield. On the other hand, when you bought the bond at Rs 1200, the current yield will be 8.3% (Rs 100 as % of Rs 1200 you spent).

Current yield = (Annual coupon rate / Purchase price) X100

One important factor you may have observed here is that there is inverse relation between bond price and bond yield (especially when you are purchasing or selling the bond in the secondary market).

The higher the price an investor pay for a bond, the lower the yield, and vice versa.

There is another type of yield concept that is called yield to maturity (YTM). Its calculation is slightly complex, and you need software to estimate it for simplicity sake we are avoiding it.

Types of yieldThere are three major types of yield: (i) Coupon Yield: The coupon yield is simply the coupon payment as a percentage of the face value. Coupon yield = Coupon Payment / Face Value Illustration: (ii) Current Yield: The current yield is simply the coupon payment as a percentage of the bond’s purchase price. Current yield = Coupon payment / Purchase price) X100. Coupon: Rs 100 (iii) Yield to Maturity: Yield to Maturity (YTM) is the expected rate of return on a bond if it is held until its maturity. Yield to maturity is often the yield that investors inquire about when considering a bond. Yield to maturity requires a complex calculation. It considers several factors including the following: § Coupon rate interest rate. § Price—the higher a bond’s price, the lower its yield. § Years remaining until maturity. § Difference between face value and price. |

Operation twist and the yield gameWhen the RBI buys long term bonds of the government, there will be high demand for long term bonds and hence their price increases in the market. (imagine that price goes up say from Rs 1000 to Rs 1050). Interest rate that the government gives remains the same (for these bonds imagine that it is 7%). Remember, there is inverse relation between price of a bond and its yield. So, as a result of the heavy purchse of long term bonds by the RBI, demand goes up, price goes up and yeild goes down. A Rs 70 interest amount in Rs 1050 investment is lower than Rs 70 interest amount in Rs 1000 investment (this means that a person who buys bonds now gets only lower return given the same interest rate but the higher price he paid for the bond). There is the trend of declining yield (what we call it as current yield). |

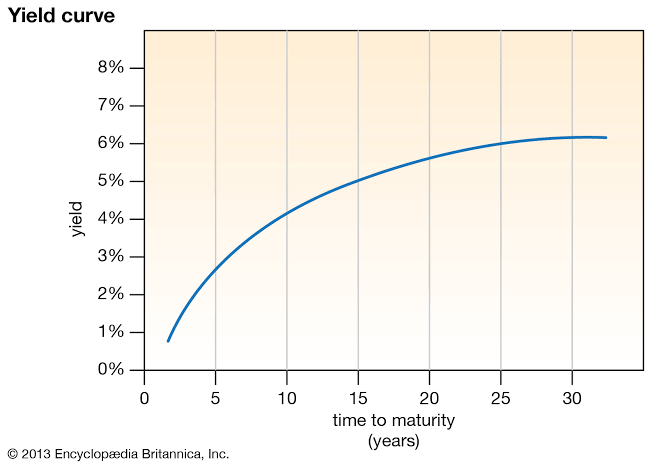

Yield Curve

The yield curve shows the relation between the (level of) interest rate (or cost of borrowing) and the time to maturity. Don’t forget to read yield as interest rate as well.

Basically, yield depends on maturity time.

Y = f (t)

In normal cases, the yield is an increasing function of time (maturity).

Higher the maturity, higher will be the yield. The meaning is simple – if a borrower would like to issue long term bonds (to borrow for long term) he should give higer interest rate compared to short term borrowings.

The curve that shows the yield for various maturities is called the yield curve.

A normal yield curve will be upward sloping. This upward sloping yield curve shows that the interest rate for short term borrowing is low whereas the interest rate for long term is high. This is because for long term, the time period is high and hence the risk is also high.

For example, if the government of India is borrowing through the issue of 364-day treasury bill, its yield will be around 5.50%.

On the other hand, if the government is borrowing by issuing a 10-year bond, the yield or interest rate will be around 6.65%.

A simple yield curve is shown below (image courtesy to Encyclopedia Britannica).

There are other types of yield curves as well; like inverted yield curve. Shape and position of the yield curve for important securities like government bonds often shows different macroeconomic situations. The types of yield curves will be covered in another session.

*********