The leading indicator to measure the size of a government’s tax revenue is the tax-GDP ratio. Actually, the tax-GDP ratio tells about the size of the government’s (central government’s or central plus states- as the case may be) tax revenue expressed as a percentage of the GDP.

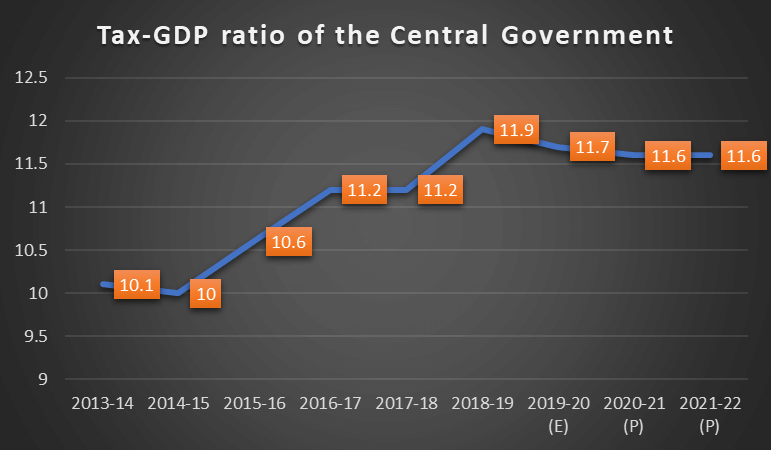

Suppose, the tax-GDP ratio of the central government is 11.7% (as per the BE of 2019-20 budget). It means that if the GDP of India is Rs 100, the tax revenue of the central government is Rs 11.7%. so, that is the size of tax revenue when compared to the GDP.

Tax-GDP ratio of the centre and states combined will be near around 16%. Big changes in tax GDP ratio rarely occurs.

Higher tax-GDP ratio is a happy situation for the government. It clearly indicates increased fiscal capacity of the in the budget to finance its expenditure. If tax-GDP ratio is higher, it will help the government to reduce its dependence on borrowings.

What should be the ideal tax -GDP ratio?

India’s tax-GDP ratio is lower compared to the international level. At the same time, India’s government expenditure to the public is also lower than the world average. Still, higher tax revenues will help the government to provide more services to the people in the form of welfare schemes.

The basic principle is that the government should get adequate revenues to finance its expenditure. Hence tax-GDP ratio should be enough to meet government expenditure.

In Western countries, the tax GDP ratio is higher. Several governments have tax-GDP ratios of nearly 20 to 25%. But at the same time, government expenditure there is also very high as those Government makes expenditure on hospital expenditure, free schooling etc.

In India, compared to several other countries, tax-GDP ratio is lower. The combined tax-GDP ratio for the canter is estimated to be around 11.7% as per 2019-20 budget.

Reasons for low tax-GDP ratio:

Tax GDP ratio is lower because of narrow tax base. Only about 4% of the country’s population pays income tax. There is large scale of tax evasion. Similarly, corporate have tendency to avoid taxes. Weaknesses in tax administration is another factor.

What are the measures for the improvement of tax-GDP ratio in India?

Over the last one decade the government has made several steps to raise tax -GDP ratio. The main hurdle is the prevalence of black economy. The demonetization programme and the follow up steps have added strength to the fight against black money. Tax -GDP enhancement steps are broadly two:

- Refining tax structure

- Improving tax administration

Refining tax structure

A simplified tax structure with optimum number of tax slabs, optimum tax rates, reduced number of concessions and deductions etc., makes low scope for tax avoidance as well as tax evasion.

Tax structure of India is already a settled one. In 2019, the corporate income tax rate has been down to 22% (aggregate 25.17%) by eliminating all concessions and deductions. The new structure avoids complexities in tax administration.

In the case of PIT, there are only three rates. Unnecessary deductions and exemptions were eliminated. But the recent creation of new tax slab of above Rs 5 crore may add to tax administration difficulties.

Regarding indirect taxes, the launch of GST is supposed to raise tax revenues once the beginning stage problems are over. Still, the low revenue realisation even into its third year of implementation is a matter of concern.

Improving tax administration

Now, tax administration is the central pillar for improving tax revenues. Several administrative measures were launched to augment tax revenue realization in recent years. Important administrative measures are:

Aadhaar – PAN linkage, use of digital technology to improve tax administration, e- way bills, Project Insight, Project Saksham, introduction of Goods and Services Tax (GST), extension of the Indian Customs Single Window Interface for Facilitating Trade (SWIFT) and other taxpayer-friendly initiatives under Digital India and Ease of Doing Business of Central Board of Excise and Customs, Tax Deducted at Source (TDS)/withholding taxes and e-TDS; presumptive taxation; adoption of a single identification number (TIN), taxation of SMEs and wealthier citizens; better tax enforcement, more demands for disclosure and transparency; review and refinement of tax incentives/exemption/deductions; tighter transfer pricing regulations and oversight; and expanding the indirect tax net over more goods and services.

According to the TARC (Tax Administrative Reforms Commission), technological innovations have helped tax administration significantly. PAN based transactions; online tax filings etc., have improved the efficiency of tax administration in the country.

*********