Joining the government to fight the economic effect of the Covid pandemic, the RBI on a war mode has declared several measures to support the ordinary people, the financial system and the economy. These includes measures including a three-month moratorium on all term EMIs, extraordinary measures to inject liquidity into the banking system, measures to check banks from being risk averters and to step up foreign currency liquidity in the economy.

Inflation may come down; food supply is stable

Another relief of the RBI’s extraordinary intervention that comes on the prediction side is that inflation may come down given the positive food production and food stock situation, crashing crude prices and lower aggregate demand in the economy. This assessment is a big assurance that is realistic, and it indicate that the nation is able to withstand the zero economic activity without causing any fear of famine and chaos.

The main relief from the ordinary man’s angle is the three-month moratorium on term EMIs. Here, the RBI extends this moratorium from commercial banks to cooperative banks and Financial Institutions.

In his vital announcement, the RBI governor clubbed several measures along with the rate cut that is usually taken by the MPC.

RBI’s Comprehensive package along with the MPC effort to support the economy from the Covid onslaught

Directly coming to the comprehensive package to fight the Covid pandemic, the RBI announced following set of measures.

- Liquidity support measures

- Regulation and supervision measures to support credit flow from the banking sector.

- Relaxation of Repayments

- Measures to improve the functioning of the financial market

- Liquidity Measures

Liquidity support: Targeted long-term repos for three years

|

(a) Targeted Long-Term Repo Operations (TLTRO)

The liquidity is in stress as there is high sell off in the equity, bond and foreign exchange markets. Hence to inject funds, the RBI will conduct auctions of targeted term repos of up to three years tenor for a total amount of Rs 100000 crores. The interest rate will be linked to the repo rate.

Banks have to deploy the funds obtained from Targeted Long-Term Repo Operations in investment grade corporate bonds, commercial paper and non-convertible debentures.

Eligible instruments comprise both primary market issuances and secondary market purchases, including from mutual funds and non-banking finance companies.

The first auction of Rs 25,000 crore will be conducted on 27th March 2020 (on the policy announcement date).

(b) Cash Reserve Ratio reduced by 1% for the next one year

|

Liquidity: CRR cut and MSF

|

Cash Reserve Ratio (CRR) of all banks is cut by 100 basis points (1%) to 3.0 per cent from March 28, 2020 for a period of one year. This is a historically low CRR unveiled by the RBI. Even during the Lehman crisis time of 2008 September, the RBI has not cut the CRR below 4%.

This cut in CRR would release primary liquidity of about Rs 137,000 crore uniformly across the banking system. Readily banks can now use this extra money to give loans.

Another related but insiginificant step is that equirement of minimum daily CRR balance maintenance by banks reduced from 90 per cent to 80 per cent, till June 26, 2020. This is due to operational inconvenience in banks out of the Covid spread.

(c) Marginal Standing Facility

The temporary one day loans to banks under the Marginal Standing Facility (MSF) will be enhanced from 2 per cent of the SLR to 3 per cent with immediate effect. This measure will be applicable up to June 30, 2020.

Total liquidity enhancement effect: These three measures relating to TLTRO, CRR and MSF will inject a total liquidity of Rs 3.74 lakh crore to the system.

(d) Repo and reverse repo cut

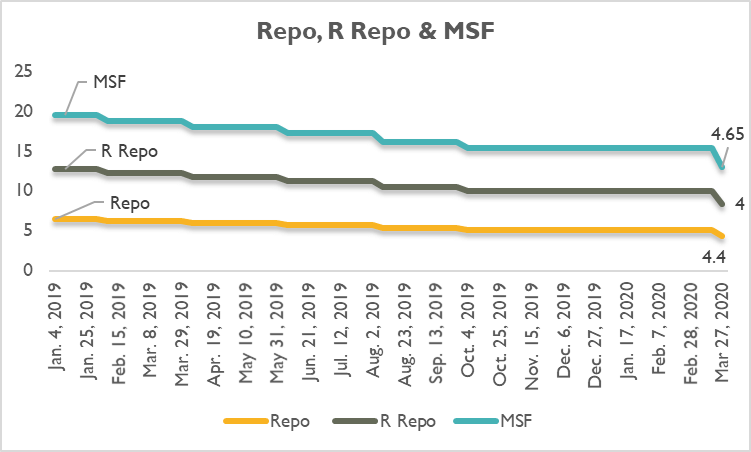

RBI’s MPC decided to cut the policy rate of repo by 75 basis points to 4.4 per cent.

| Repo cut by 75 bps and reverse reop by 90 bps: meaning

The repo rate has been reduced by 75 bps. But a higher cut has been announced in reverse repo (90 bps). The meaning is that if the banks parks funds with the RBI through Reverse repo, there will be much less interest rate (interest rate for reverser repo cut by 90 bps). So, banks are discouraged to park funds with the RBI under the reverser repo window. The RBI observed that banks’ lending to the RBI through reverse repo increased since the start of the Covid crisis. Banks are not ready to give loans to the public rather is keeping cash with the RBI to avoid risk. “The purpose of this measure relating to reverse repo rate is to make it relatively unattractive for banks to passively deposit funds with the Reserve Bank and instead, to use these funds for on-lending to productive sectors of the economy.” |

In the same way, Reverse repo rate reduced by 90 basis points to 4.0 %. More reduction in Reverse repo rate will discourage banks to park money with the RBI. So, banks should not be risk averse.

The asymmetrical corridor to discourage banks to park funds with the RBI

A curious outcome of the new bigger cut in reverse repo rate is that the so-called corridor or the gap between the reverse repo rate and the Marginal Standing Facility Rate has been widened.

During March so far, banks have been parking close to Rs 3.2 lakh crore on a daily average basis under the reverse repo, though the growth of bank credit has been slowing down.

Widening of the Monetary Policy Rate Corridor. In view of persistent excess liquidity, it has been decided to widen the existing policy rate corridor from 50 bps to 65 bps. Under the new corridor, the reverse repo rate under the liquidity adjustment facility (LAF) would be 40 bps lower than the policy repo rate, as against existing 25 bps. The marginal standing facility (MSF) rate would continue to be 25 bps above the policy repo rate.

Figure: the corridor – Reverse repo and MSF as per the new policy delaration from March 27, 2020

- Loan relief- moratorium on repayment etc. (Regulation and Supervision)

As a result of the pandemic, debt repayment will be slowed. Hence banks may come under stress. But the transmission of financial stress to the real economy has to be checked.

Banks should be supported to provide relief to borrowers in these extraordinarily troubled times. Towards this, the RBI extends several measures:

- moratorium on term loans;

- deferring interest payments on working capital;

- easing of working capital financing;

- deferment of implementation of the net stable funding ratio; and

- the last tranche of the capital conservation buffer.

Moratorium on Term Loans for three months

All commercial banks (including regional rural banks, small finance banks and local area banks), co-operative banks, all-India Financial Institutions, and NBFCs (including housing finance companies and micro-finance institutions) (“lending institutions”) are being permitted to allow a moratorium of three months on payment of instalments in respect of all term loans outstanding as on March 1, 2020.

Deferment of Interest on Working Capital Facilities

For the working capital facilities sanctioned in the form of cash credit/overdraft, lending institutions permitted to give a deferment of three months on payment of interest in respect of all such facilities outstanding as on March 1, 2020. The accumulated interest for the period will be paid after the expiry of the deferment period.

The moratorium on term loans and the deferring of interest payments on working capital will not result in asset classification downgrade.

None of these will be counted as default and credit information and rating will be neutral without any adverse impact on the credit history of the beneficiaries.

Deferment of Implementation of Net Stable Funding Ratio (NSFR)

The implementation of NFSR requirement for banks will be deferred by six months to October 1, 2020.

Deferment of Last Tranche of Capital Conservation Buffer

The date of implementation of the capital conservation buffer (CCB) under Basel III norms is deferred from March 31, 2020 to September 30, 2020.

III. Financial Markets

The measure for financial markets assumes importance in the context of the increased volatility of the rupee caused by the impact of Covid-19 on currency markets.

Permitting Banks to Deal in Offshore Non-deliverable Rupee derivative Markets (Offshore Rupee NDF Markets)

Banks in India which operate International Financial Services Centre (IFSC) Banking Units (IBUs) are now allowed to participate in the overseas NDF market with effect from June 1, 2020. This will give banks more access to currency derivative markets.

RBI will use both conventional and non-conventional methods to fight Covid

The RBI will continue to remain vigilant and will take necessary steps to mitigate the economic impact of COVID-19 and preserve financial stability. All instruments – conventional and unconventional – are on the table for the RBI.

Since the last MPC meeting of February 2020, the Reserve Bank has injected liquidity of Rs 2.8 lakh crore through various instruments, equivalent to 1.4 per cent of our GDP. Together with the measures announced today, RBI’s liquidity injection works out to about 3.2 per cent of GDP.

Also Read: What is RBI’s Monetary Policy Corridor?