In the Budget 2022, Finance Minister Nirmala Sitharaman proposed taxation of the newly emerging asset class of crypto assets by forging a category called Virtual Digital Assets and providing a definition to such assets. The intervention thus effectively addressed one of the leading issues related with crypto assets- taxation.

What are Virtual Digital Assets?

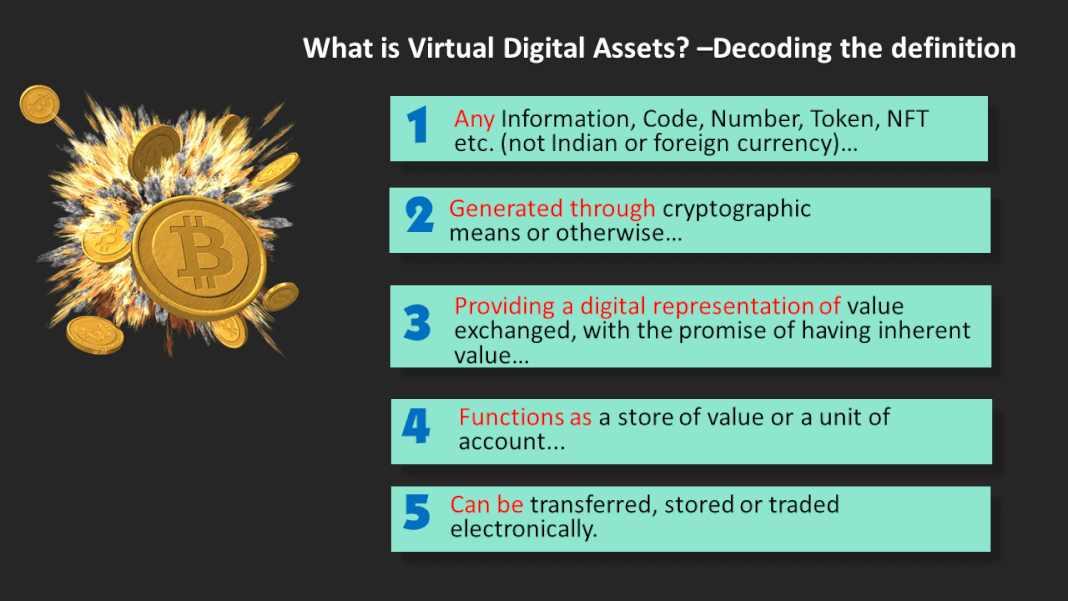

Virtual Digital Assets covers any information, code, number or token, non-fungible token etc (that is to be notified by the government), created through a cryptographic process and provide a digital representation of value exchanged, with the promise of an intrinsic value. Such assets can be transferred, stored or traded electronically.

Definition of Virtual Digital Assets under the Income Tax Act (in detail)

The Clause 47A of the Income Tax Act, introduced under section 2 defines Virtual Digital Assets.

(a) any information or code or number or token (not being Indian currency or foreign currency), generated through cryptographic means or otherwise, by whatever name called, providing a digital representation of value exchanged with or without consideration, with the promise or representation of having inherent value, or functions as a store of value or a unit of account including its use in any financial transaction or investment, but not limited to investment scheme; and can be transferred, stored or traded electronically;

(b) a non-fungible token or any other token of similar nature, by whatever name called; Report this ad (c) any other digital asset, as the Central Government may, by notification in the Official Gazette specify.

The Central Government may, by notification in the Official Gazette, exclude any digital asset from the definition of virtual digital asset.

*********

Act 2015?")