When symptoms for a deep slowdown is increasingly evident, the economy badly need some intervention from the government. The usual fiscal stimulus in the form of increased expenditure and tax cuts are the textbook interventions.

Higher expenditure by the government is the conventionally adopted medicine to fight the slowdown. In the same way, reduction of tax rates especially in key sectors including automobile encourages consumer expenditure.

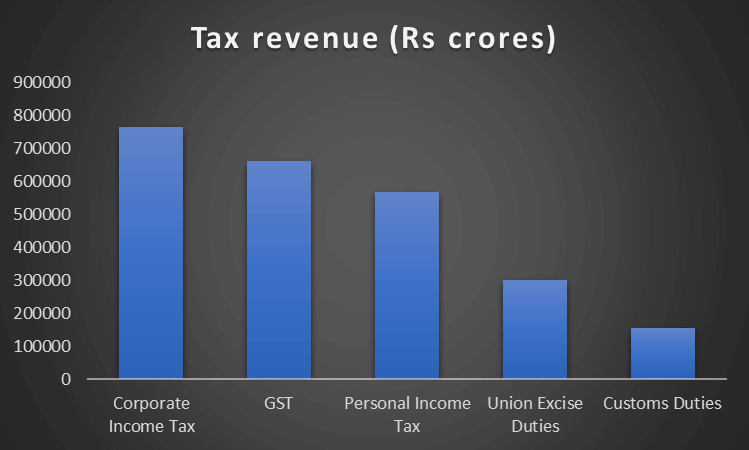

But the current fiscal situation makes it tough for the government for substantial tax cuts. Already, the GST shows a sorry figure from the angle of tax revenue realization. The GST is lower by nearly Rs 1 lakh crore vis a vis corporate income tax.

Declining sales means lower tax revenue for the government

More than that, once the sales and thus profits of companies start to come down, the government’s largest tax revenue- the Corporate Income Tax is expected to register a sizable fall. This is the fear factor as CIT is the biggest contributor to the government purse.

In the last budget, Finance Minister Nirmala Sitharaman assumed a tax revenue growth of 10 %. Some taxes like the Personal Income Tax is assumed to get very high growth rate. The Central Board of Direct Taxes (CBDT) targeted 19% per cent increase in personal income tax.

With the slowdown in economic activities, sales, income and taxes are expected to fall sequentially. So, the biggest central taxes – the CIT, GST and the personal income tax are expected to register revenue shortages compared to the budget targets.

Table: Tax revenue estimated – Budget 2019 (July)

| Tax | Amount (Rs crores) | Percentage share in total tax revenue |

| Corporate Income Tax | 766000 | 30 |

| GST | 663343 | 26 |

| Personal Income Tax | 569000 | 22.3 |

| Union Excise Duties | 300000 | 11.75 |

| Customs Duties | 155904 | 6.1 |

| Gross Tax revenue of the centre | 2552131 | 100 |

Disinvestment target may not be realised

Another receipt shortage may come in the form of unrealised disinvestment receipts. Since the economy is in the downturn, bidders may not show interest in disinvestment. The target for disinvestment is Rs 105000 crores; that is a historical high.

A major portion of this revenue is supposed to come from strategic disinvestment where bulk money is expected to get from selling PSEs. But, given the empty pockets of corporates, their risk averse mentality, financial sector weaknesses and the general pessimistic business mood, disinvestment is going to be a tough exercise.

There is every chance that disinvestment assets may go under-priced when they are sold in a weakening economy.

Tax cuts are difficult to be made

Given the precarious fiscal situation of the government, the scope for tax cuts to stimulate demand, is difficult to undertake. Any tax cut means revenue shortfall and inability of the government to finance its expenditure.

So, both tax cuts and expenditure augmentation have limitations in the present context, and it limits government’s ability to boost the economy.

*********