Local Currency Settlement of international transactions is going through a boom phase now. China started the trend of Local Currency Settlement System (LCSS) in 2009 and several other countries are following the Chinese model. In a significant step, India recently signed an LCSS with the UAE, and this is of tremendous importance as India-UAE trade amounts to nearly $85 billion and UAE is the third largest trade partner for India after the US and China. An LCSS with UAE implies that $85 billion worth of US Dollar use is avoided from India’s trade engagements. Investment and remittance settlement implications under the India-UAE LCSS is outside this estimate.

What is Local currency settlement System (LCSS)?

The Local Currency Settlement System (LCSS) is a cross border payment mechanism which allows trading entities from two countries to make payments in their own national currencies. Unlike the multilateral settlement system that is followed under the Bretton Woods System, the LCSS are largely bilateral agreements and arrangements, (exception -involving trade blocs).

Under LCSS, in contrast to the existing practice of using a reserve or hard currency like the US Dollar, payments for imports and exports are done through the currencies of the respective trade partners. The word ‘local’ should be read as ‘national’.

The Ministry of Finance, Government of India, defines the LCSS from the Indian angle: “the INR / Local currency settlement mechanism aims at putting in place a form of payment arrangement for trading partner countries of India to raise their invoices and receive payments in their respective home currency. The INR / Local currency settlement mechanism has been designed for the settlement of bilateral trade transactions between India and its trade partner countries, whereby both countries settle payments for their trade transactions on bilateral basis in INR / Local currencies.”

Why the mushrooming of LCSS?

Several developments in International Monetary System (IMS) including appreciation of the US Dollar, US Fed’s monetary policy decisions and its impact on emerging market currencies, trade frictions between the US and China, attempts of major non-European countries to avoid overreliance on Dollar etc. have contributed to this trend of local currency settlement.

Why is Local Currency Settlement Mechanism (LCSM) gaining popularity now?

A large number of factors are compelling emerging market economies to opt for local currency settlement mechanisms during the last few years.

- Transaction costs of payment will come down: LCSS eliminates the cost of exchanging domestic currency with the international reserve currency like the US Dollar. The involvement of such a third-party currency indeed raises transaction cost of the trade. Weaknesses in International Monetary System in recent years also encouraged the faster spread of LCSS culture.

- The risk of quick capital outflows from the EMEs, due to the US Federal Reserve’s monetary policy decisions: Over the last couple of years, the monetary policy stance of the US Federal Reserve has created fluctuations in the exchange rate of several Emerging Market currencies. Hence, continuous reliance on US Dollar will make domestic exchange rate vulnerable. Lower use of the US Dollar and thus lower reliance on it will reduce the adverse impact of US monetary policy on domestic exchange rate.

- Sanctions and other political issues will not affect payments: The Western sanction on Russia, whatever may be its good objective raised eyebrows and proved that currency and payment related sanctions by the West can harm the interest of countries during adverse times. Here, local currency settlement helps to avoid the adverse effects of such sanctions. An interesting point here is that several countries including India are promoting cross national payments using their digital platforms (e.g. India-UAE payment agreement using the UPI).

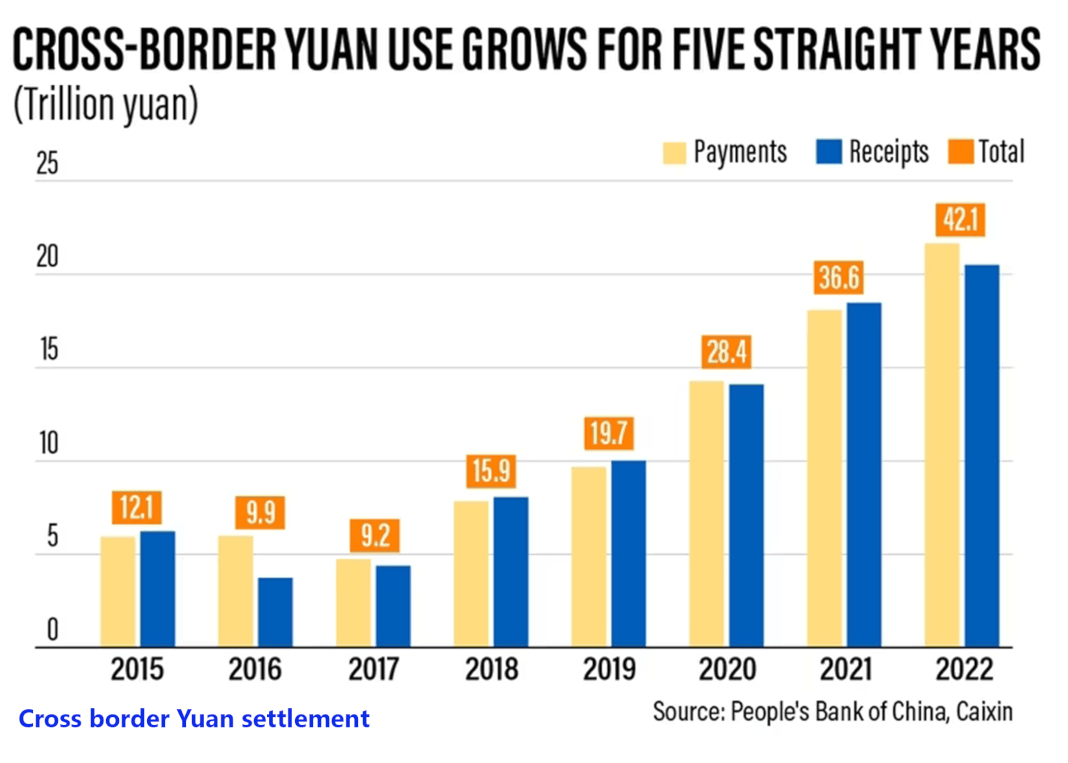

- China’s Success story in LCSS: Success of countries like China who adopted LCSS in the past is a motivation, China’s Renminbi payment was around 42.1 trillion yuan or ($6.3 trillion) in 2022, up from just 3.6 billion yuan in the second half of 2009.

- Internationalisation of domestic currency: LCSS helps national currencies to get higher international status. Trade in the concerned domestic currencies will go up with LCSS.

- Trade and investment will be encouraged with easier and less costly payment settlements. The LCSS will also help to develop forex markets in both countries.

Figure: Growth of China’s Local Currency Settlement turnover

Working of the Local Currency Settlement System – an Example

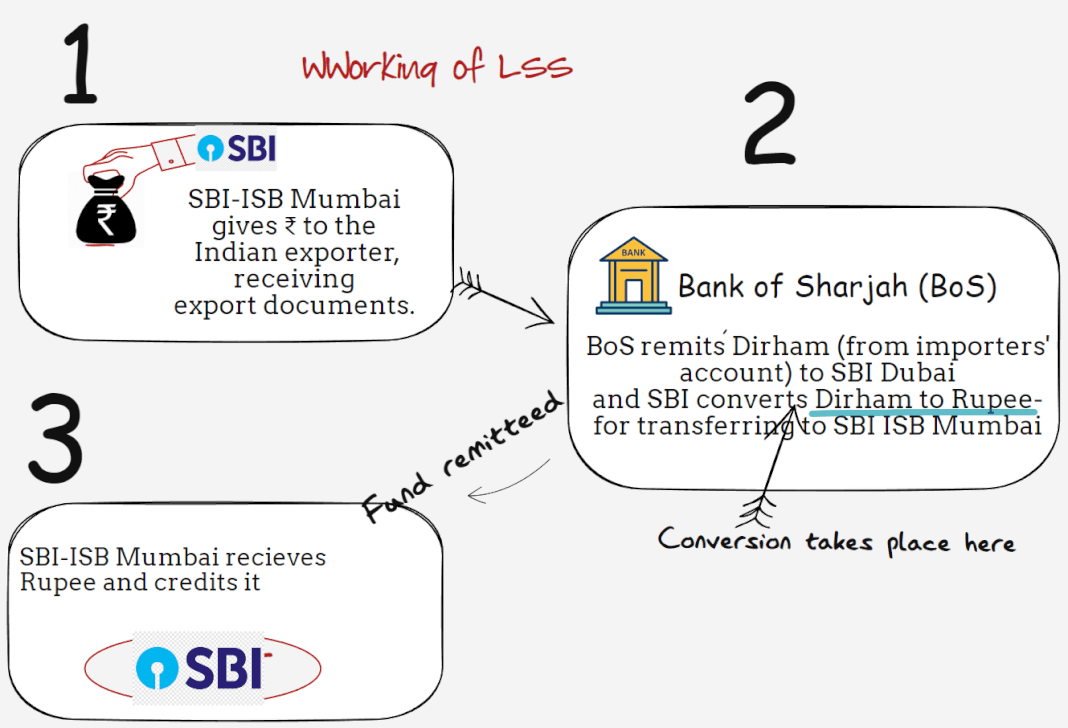

An illustration will help to understand the working of LCSS. Already, an LCSS agreement has been signed between India and the UAE. Imagine that the SBI is the designated indian bank under the LCSS, whereas the Bank of Sharjah (BoS) is the designated UAE Bank (there can be large number of banks and involvement of the foreign exchange market).

An indian exporter from Mumbai makes exports to the Dubai (UAE). As a first step, the exporter gets his payment in Indian rupees from the designated indian bank (SBI-ISB (International Services Branch), Mumbai) for the exports made to an importer in Dubai (UAE). Then, as a next step, SBI-ISB sends the documents to its designated UAE Bank – the Bank of Sharjah (BoS). The Bank of Sharjah exchanges equivalent UAE Dirham (AED) to the SBI’s branch in Dubai for conversion into Indian rupee. As a next step, the SBI branch in Dubai makes payment to the SBI-ISB in Mumbai. There is no involvement of any hard currency like the US Dollar. The exporter gets his payment in India in Indian rupees.

Figure: Working of India’s proposed LCSS with UAE illustrated.

The core part of this exchange that involves the currency payment is the Dirham (AED) to Rupee conversion made by the SBI branch in Dubai. It gets the AED and may exchange the AED into Rupee in the Dubai international currency exchange. Indeed, this requires higher level rupee trade and trading arrangement in the Dubai International currency exchange. As part of the India-UAE, Local Currency Settlement, both countries aim to promote INR-AED trade in their respective forex markets.

Objectives of LCSS: Government of India

The Ministry of Finance in its circular to the Public Sector Banks, regarding the LCSS, has pointed out following objectives from India’s LCSS with UAE

(i) To provide a bilateral facility for settling payments in home currency regarding current account transactions between India and the trading partner countries.

(ii) To promote the use of domestic currencies of the partner countries in current account transactions.

(iii) To promote co-operation and closer relations among the banking systems of the two countries, and thus expansion of trade and economic activity between the two countries.

(iv) To encourage the exporters / sellers of the two countries to use the home currencies and thereby eliminating exchange-risk and thus discovering competitive pricing.

Sources:

1. Asian Development Bank on LCSS

2. Ministry of Finance, Government of India.

?")