India has been trying hard to modify and modernise the six-decade old Income Tax Act for the last several years. Attempts were made previously to bring a Direct Tax Code (DTC). Still, several issues blocked the design of such a big law to replace the mammoth Income Tax Act that was drafted in 1961.

But this time, in the 2020 budget, it is expected that there is every chance for the old law to be scrapped. In its place a new Direct Tax Code (DTC) is to be inducted. The task force on DTC’s recommendations to the government on August 18, 2019 added additional element to the budget.

Most importantly, the task force has also provided a draft law for replacing the 1961 Income Tax Act. The IT Act covers several taxes including personal income tax, corporate tax and levies such as capital gains tax, dividend distribution tax etc.

What is Direct Tax Code (DTC)?

Direct Tax Code is set of rules that is going to replace the existing Income Tax Act (IT Act). It covers all taxes that is under the present IT Act including corporate income tax and personal income tax. Effort to create a DTC started from 2009 onwards.

Why DTC?

The most important reason for scrapping the Income Tax Act is that it is age-old and complex. It has nearly 700 sections. Economic and business environment has changed big since 1961. The Vodafone case where the government lost battle at the supreme court is a classic example for the lack of flexibility of the IT Act . Prime Minister Narendra Modi, in 2017, had observed that the Income-Tax Act, 1961, was drafted more than 50 years ago and it needs to be redrafted.

The government appointed a task force on Direct Tax Code in September 2017, ‘to draft new income tax legislation for India in “consonance with the economic needs of the country.’

| Direct Tax Code – Brief History

· The first Draft Direct Taxes Code Bill was released on August 12, 2009, · Revised Discussion Paper (RDP) was created in 2010. · DTC 2010 was introduced in Parliament. · A Standing Committee of Finance (SCF) was appointed to discuss it with various stakeholders. · The SCF submitted its report to Parliament in 2012. · A ‘revised’ version of DTC was released in 2014 after the report by the SCF. · Later it was lapsed with the change in government. · In 2017, NDA government set up an expert committee to draft a new Direct Taxes Code. · Report of the task force on DTC was submitted to Finance Minister Nirmala Sitharaman on August 19, 2019. · Budget 2020 is expected to take steps to implement the DTC. |

Task of the committee

Main recommendation of the committee was to make the I-T Act simpler, with focus on easing the burden on individuals and companies so that economic growth can be supported with incentives and easing of economic activities.

The task force was assigned to design direct tax laws by considering the standards prevailing in other countries. It hast to incorporate international best practices, at the same time keeping in mind the economic peculiarities of the country.

Composition of the Task Force

The taskforce was originally led by Arbind Modi but was later replaced (after the retirement of Sri Modi) by Akhilesh Ranjan (convenor), who is a CBDT member.

Other members of the eight-member task force include Girish Ahuja (chartered accountant), Rajiv Memani (Chairman and Regional Managing Partner of EY), Mukesh Patel (Practicing Tax Advocate), Mansi Kedia (Consultant, ICRIER) and G C Srivastava (retired IRS and Advocate).

The taskforce submitted its recommendations on august 19, 2019.

According to press information, the report has two parts:

(1) Recommendations and

(2) Draft Bill.

The Ministry has kept the report in secret and hence details of the report is not available in the public domain. Finance Ministry is believed to be working on the report for its implementation through budget 2020.

Importance of the Task Force’s recommendations

The Finance Ministry in its statement said that the committee submitted its report on replacing the Income Tax Act with a new Direct Tax Code. Since the current Income Tax Act was passed in 1961, it needed a significant change in the context of the changed circumstances. Hence, the DTC was inevitable. Still, efforts to launch the DTC was there since 2010; but there was only limited success.

The Taskforce report brings tax law

Main feature about the taskforce report is that it is not just a report as it brings a draft law along with the report. The task force brought a new income tax law with over 300 sections with minute details. Existing IT Act has nearly 700 sections. According to tax experts the ambition of such an effort is ‘simplification and removal of ambiguity.’

The task force is believed to have made several recommendations that is aimed to reduce the tax complications for the individuals as well as that for the corporate. It has highlighted the need to review existing tax brackets, surcharges and implementation of special guidelines for start-ups.

For individuals: the task force recommended simplification and rationalisation of the tax slabs and elimination of excess surcharges.

For companies: the task force suggested uniform tax rate for domestic and foreign companies. It also recommended a branch profit tax for repatriation of profit and other income by foreign companies from India. The task force also recommended special provisions for start-ups.

Another recommendation is the abolition of dividend distribution tax for companies. Detailed report of the task force is not published by the government. Still, some recommendations are leaked to the media and is widely shared.

Following are the main recommendations of the Task force on DTC

- Personal Income Tax: simplification of personal income tax structure

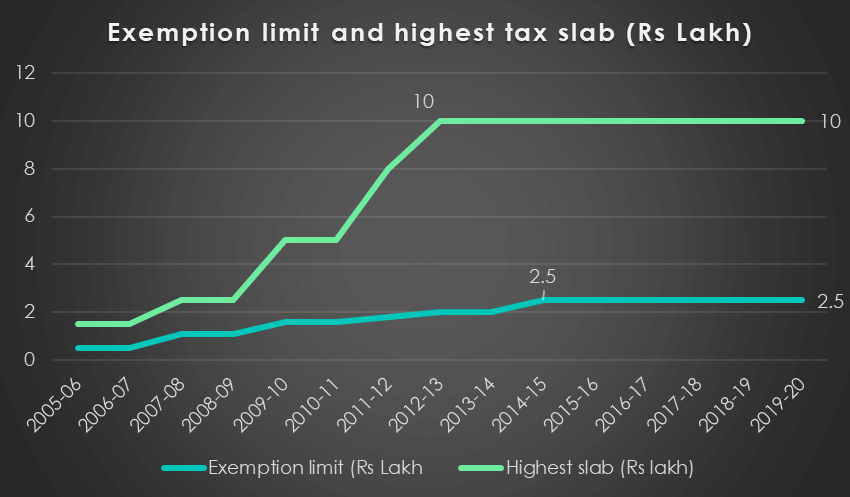

The popular recommendation of the task force is regarding personal income tax structure. Slabs and rates are remaining constant for several years though some ad hoc changes in the form of rebate, standard reduction etc occurred from lower tax slabs.

Figure: Unchanged exemption limit (Rs 2.5 lakh) and the higher income tax slab (Rs 10 lakh and above) for the last several years.

Here in this context, the task force tries to rationalise personal income tax slab. raising the tax slab and reducing the tax rate will give big relief to the middle-class taxpayers. In conclusion, the DTC will the tax law that India’s middle class is looking for. The new slab and rates are as following.

| Slab | Rate | Remark |

| Below Rs 2.5 lakh | Nil | |

| Rs 2.5 lakh to Rs 10 lakh | 10% | With a full rebate upto Rs 5 lakh |

| Rs 10 – 20 lakh | 20% | |

| Rs 20 lakh to Rs 2 crores | 30% | |

| Rs 2 crore plus | 35% |

- Uniform corporate tax for domestic and foreign companies

At present, there is different corporate income tax for domestic companies (25.17%) and foreign companies (40% plus surcharge and cess). This tax rate is among the highest in the world. Hence, the task force suggested for imposing uniform tax rate.

- Abolition of Dividend Distribution Tax (DDT)

The task force recommended the abolition of DDT. At present domestic companies have to pay a tax of 20.65% on the dividend distributed to their investors.

| What is Dividend Distribution Tax?

Dividend Distribution Tax is a tax imposed on dividend distributed by companies to their investors. DDT is 15 % on the amount of dividend and including surcharge and cess it comes to 20.56%. Dividend Distribution Tax was introduced in 1997. Dividend distribution tax is given by the corporate when they are distributing dividend income to investors. At the same time, individuals have to pay a tax of 10% on dividend over Rs 10 lakh they received. |

- Branch Profit tax

Foreign companies have to pay a repatriation tax in the form of branch profit tax on the earnings they repatriate to their overseas parent company. This branch profit tax will be in addition to the corporate tax they pay to the government. The proposed branch profit tax is in the spirit of the US Act – Tax Cuts and Jobs Act that encourages US companies to directly bring overseas profit to the US than to shifting them to tax havens.

- Assessing unit instead of assessment officer

Harassment by tax officials is a major defect of the present regime. Hence, instead of assessment officer, assessment units will be created to deal with individual taxpayers.

For corporate taxpayers also there will be assessment units including multiple officers along with industry specialists. All communication between taxpayers and taxmen will be digital.

- Mediation between CBDT and the taxpayer

The task force recommends a new concept of mediation between taxpayer and CBDT to reduce the volume of litigations.

- Litigation Management Unit

Deviating from the current practice, the Task Force is recommended a separate Litigation Management Unit to manage the entire tax litigation process. The litigation unit should engage in issues ranging from deciding in which cases the appeals ought to be filed to devising the strategy to defend a case.

- Public Ruling Option for Taxpayers

A concept of “public ruling” has been recommended by the taskforce. Here, taxpayers will have the option of approaching the Central Board for Direct Taxes (CBDT) for clarification on any important point of law that is not case or fact specific.

These are the main recommendations of the task force. Details about these recommendations are expected to come along with the budget (2020) statement.

*********